Entertainment, Technology & Services (ET&S)

Sales are expected to be higher than the August forecast due to the impact of foreign exchange rates, partially offset by a decrease in sales of televisions and smartphones resulting from lower unit sales. The forecasts for operating income and Adjusted OIBDA remain unchanged from the August forecast due to the positive impact of foreign exchange rates, substantially offset by the impact of the above-mentioned decrease in sales of televisions.

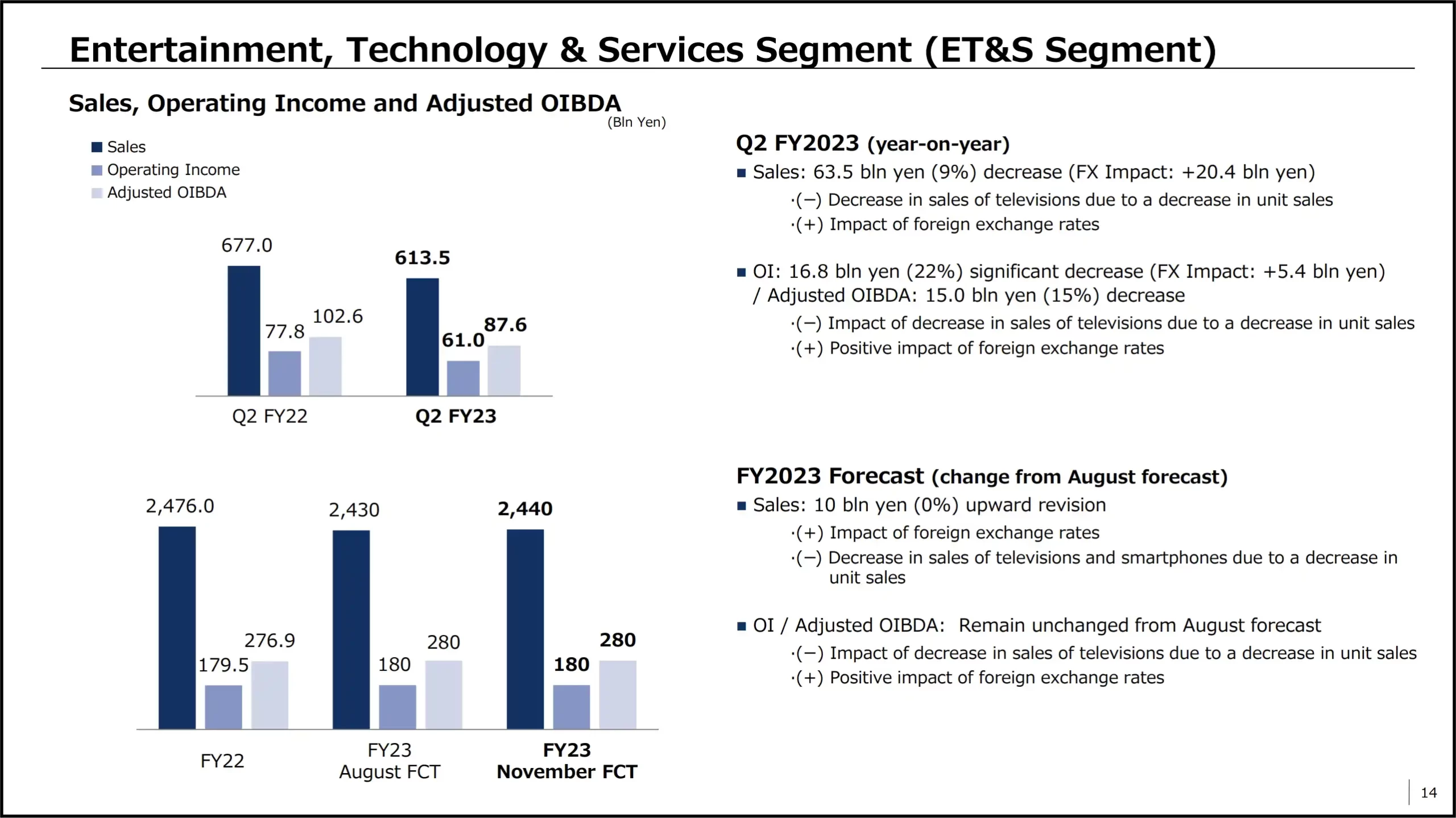

• Sales for the quarter were 613.5 billion yen, down 9% from the same quarter of the previous fiscal year in which demand for TVs increased due to a recovery from lockdowns in Shanghai.

• Operating income significantly decreased 16.8 billion yen year-on-year to 61.0 billion yen mainly due to the impact of the lower sales of TVs.

• Adjusted OIBDA decreased 15.0 billion yen billion yen year-on-year to 87.6 billion yen.

• FY23 sales are expected to be 2 trillion 440 billion yen, an increase of 10 billion yen from the previous forecast and the forecasts for operating income and adjusted OIBDA remain unchanged at 180 billion and 280 billion yen, respectively.

• The market environment for major product categories during the current quarter continued to be difficult for televisions, while products such as digital cameras and headphones remained strong.

• Regarding televisions, in response to sluggish demand and increasing price competition, we are proactively revising our sales plans conservatively and controlling sales risks and inventory risks, as well as focusing on cost reduction measures.

• Regarding the digital camera market, especially in China, which is strong, we will aim to maximize sales and profits during the year-end selling season and further expand market share in each region through the sales of new mirrorless single lens cameras and interchangeable lenses which we introduced in the current quarter and October, and which are selling well.

• Regarding inventory levels, we have thoroughly managed everything from production to sales, and we have further reduced inventory levels compared to the same period of the previous fiscal year, across all our major product categories, and have been able to control inventory at appropriate levels.

Imaging & Sensing Solutions (I&SS)

Sales are expected to be higher than the August forecast mainly due to the impact of foreign exchange rates, partially offset by an expected decrease in sales of image sensors for automotive and for industrial and social infrastructure. Operating income and Adjusted OIBDA are expected to be higher than the August forecast mainly due to the positive impact of foreign exchange rates and cost reductions, partially offset by the impact of the abovementioned expected decrease in sales.

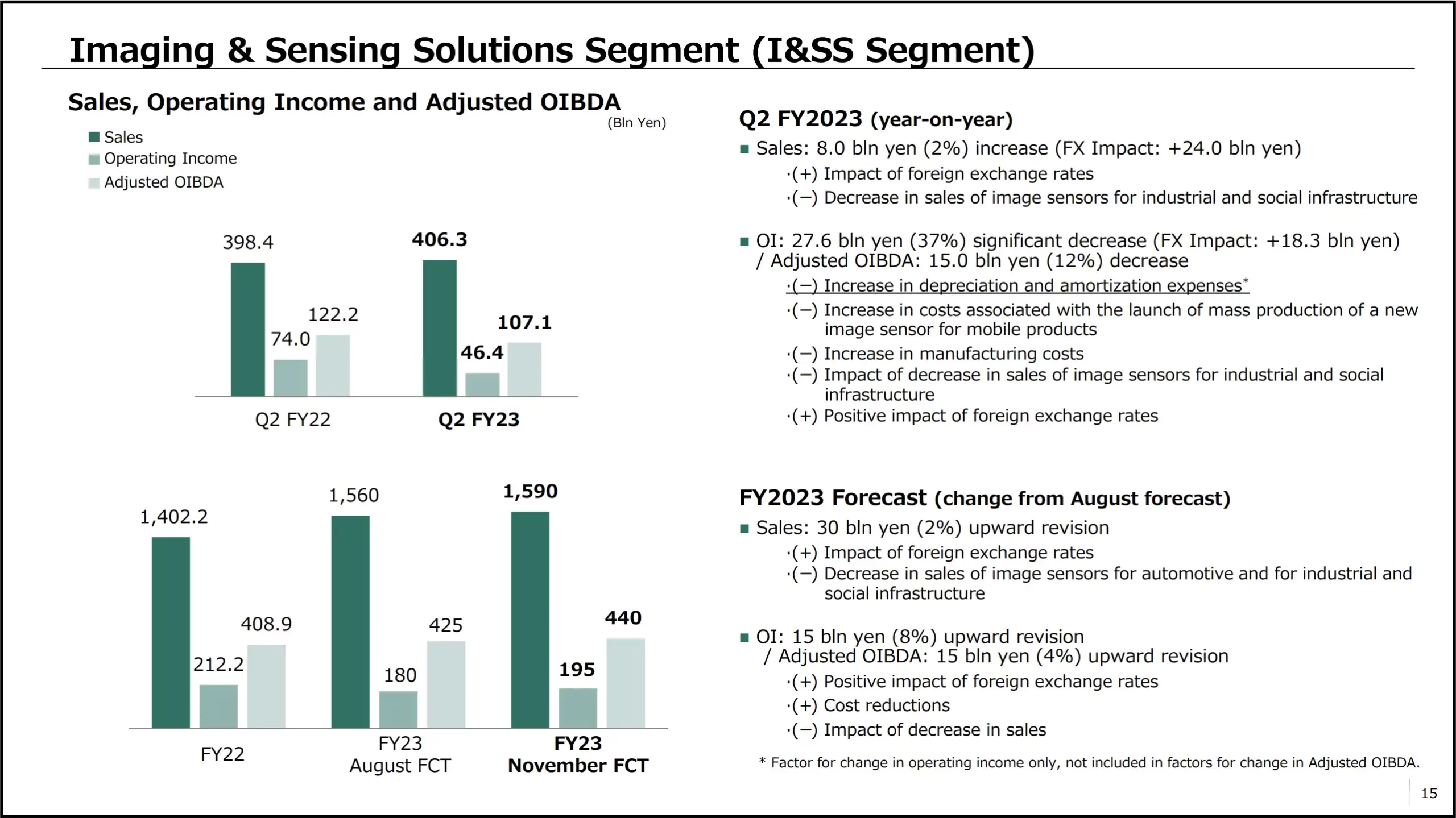

• Sales for the quarter increased 2% year-on-year to 406.3 billion yen.

• Operating income decreased significantly by 27.6 billion yen year-onyear to 46.4 billion yen, mainly due to an increase in expenses including depreciation and amortization expenses, despite the positive impact of foreign exchange rates.

• Adjusted OIBDA decreased by 15.0 billion yen year-on-year to 107.1 billion yen.

• FY23 sales are expected to be 1 trillion 590 billion yen, an increase of 30 billion yen from the previous forecast, and operating income and adjusted OIBDA are expected to be 195 billion yen and 440 billion yen, respectively, an increase of 15 billion yen each.

•In the smartphone product market, although we see signs that the demand decline is bottoming out in China and emerging markets, the North American market shows a significant year-on-year decline, and at this point, there is no change to our view that a recovery in the market will take place from next fiscal year.

• Smartphone manufacturers are incorporating larger die-sized sensors into their new products, mainly at the high-end, and the mobile sensor market by value, driven by this, is expanding as expected.

• Regarding the yield rate of our new mobile sensor product, we have achieved a certain level of improvement through the initial measures taken so far, and although unit shipments are increasing, the impact on profit remains unchanged from the previous assumption and is expected to push down the operating income forecast of the segment for the fiscal year by approximately 15%.

• Regarding automotive sensors, the market as a whole continues to show high growth due to the normalization of the supply chain and the progress of electrification in the automotive industry, but intensifying competition in the Chinese market is resulting in some of our customers capturing a low share. This, combined with the fact that the shift to higher ADAS functionality by our major customers is slower than we expected, has resulted in us slightly revising downward our forecast for the current fiscal year.

• Furthermore, regarding the image sensor market for industrial and social infrastructure, we have further reduced our forecast for this fiscal year mainly due to the effects of the slow economic recovery in China.

• Despite these factors, by incorporating the positive impact of foreign exchange rates and additional cost reduction measures, we have upwardly revised our operating income forecast for FY23 for the segment.

Follow SonyAddict on Facebook, Twitter, Instagram, and YouTube

Plus, our owners’ groups

Sony a1 Owners Group

Sony a9 Owners Group

Sony a7 Owners Group